I have insurance!! Why did I still get this bill????

We know how frustrating it is to get those bills that we were not expecting. Yes, we know…You pay almost $900 per month for your insurance plan and you just got hit by a $1000 bill! WHY???

Health care financial FAQs

Read on as we attempt to simplify and break down the complicated world of health insurance…..

What does a covered service mean?

This simply means that your insurance carrier has agreed to cover the service. It can be confusing because “covered” statement can imply that you are no longer responsible for the charges associated with the service. “Covered” simply means that your insurance carrier agrees that the service provided is within the scope of the contract between the insurance carrier and the practice.

How come I still got a bill from the practice even though the services are stated as “covered”?

The bill that you receive could be due to any of the below reasons despite the service being covered.

Co-pay: Your particular plan may have a certain amount of co-pay associated with different types of visits. For example, you may have differing co-pays for an office visit with a specialist, a primary care physician, an ER visit or a hospital visit.

Co-insurance: This is another caveat that you may not know about. Certain plans pass on a portion of financial responsibility to you as a subscriber in the form of co-insurance. This amount may also vary according to the type of visit as above and according to the type of plan.

Deductible: Most insurance carriers have a certain amount of deductible that is required to be met before they start paying out towards your visits. Just like when you have car insurance and you get into an accident. For example, if your plan has a deductible of $5000 and your car repair bill comes out to be $15,000. You will need to pay $5000 out of your own pocket first and then the insurance carrier will be the remaining $10,000. This seems unnerving and scary. However, that’s how the insurance industry works and tries to give you low-cost plans by keeping high deductibles.

You can choose to keep your deductible low by paying a higher monthly premium. It is a choice that you have to make. If you are a healthy young person who might not need a lot of visits with your doctor, you may choose a low premium, high deductible plan.

On the other hand, if you have multiple health conditions that require frequent visits, multiple medications etc., then you may choose a high premium, low deductible plan.

Ultimately, there are no free lunches in the world and you will be financially responsible for some portion either way unless you are eligible for a completely government funded plan such as straight Medicaid. Eligibility for straight Medicaid depends on your income level, number of dependents and your particular state.

My employer pays for my insurance. Why do I still get a bill?

The affordable care act made it mandatory for your employer to contribute a certain amount towards your health care costs. The employer responsibility varies from the size of the company, the type of company and may also depend on state specific laws.

Most employers will cover a portion of your health care premium and deduct the employee portion from your salary. You will see that as a line item in your pay-stub. Remember to ask your HR department at the time of onboarding to understand your contribution vs. your employer’s contribution.

I received a “bill” from my insurance? It states that this is an EOB. What is an EOB?

Insurance company never sends you a bill. They send you something called an EOB.

An EOB stands for “Explanation of Benefits”. Read carefully, at the bottom of that statement, there will be something that states, “This is not a bill”.

It is simply a statement explaining the below items:

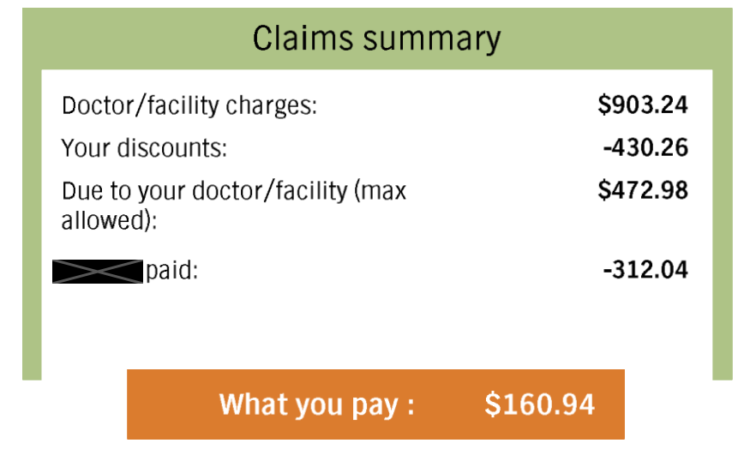

- Charges billed by your provider to the insurance: These are sometimes quite high but this does not indicate how much the provider gets paid.

- Amount the plan paid your provider.

- Amount not covered by the plan (you may or may not be responsible for this portion depending on your particular plan).

- Amount you owe your health care provider: Again, this depends on your particular plan.

Remember this is only a statement; you will receive a separate bill from your health care provider or the lab if you owe something according to your specific plan. Do not pay the insurance carrier for this. Wait for a bill. If you have questions regarding your EOB, you should call your insurance carrier directly.

Why do I get surprised by these high amounts of extra charges coated in the guise of copay, co-insurance and deductible even though I pay a huge amount of premium towards my health insurance every month?

Well, that’s because the insurance companies are trying to offer you a range of plans that you can afford. Unfortunately, everything comes with a cost. If you have a low-cost plan with a low monthly premium, your deductible and co-insurance might be very high. In such cases, you better hope that your car doesn’t get into accident or you don’t get sick. However, health care can be tricky and almost all of us will require to seek care at some point in our lives. All you can do is be fully aware of the fine print that states the charges that you might be responsible for in addition to your monthly premium.

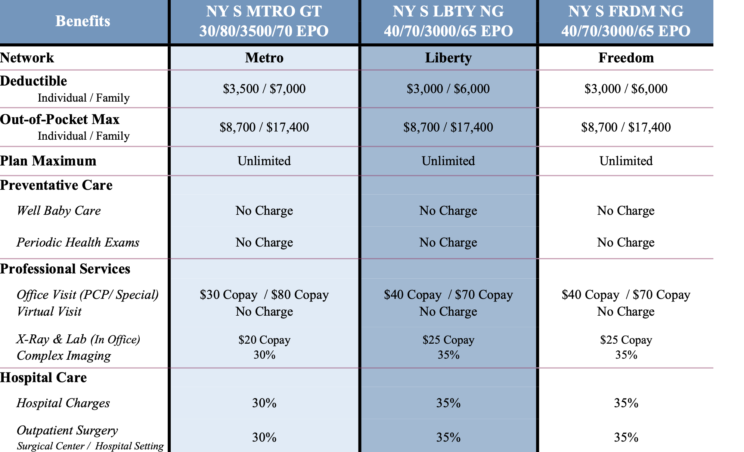

Sample insurance worksheet. Pay careful attention to yours.

I was told that I get a “free” visit once a year. What does that mean?

During the implementation of the Affordable Care Act, there was heavy emphasis on coverage of a preventative care visit or a wellness visit for all patients. All insurance carriers were required to build coverage for these visits in their plans.

An annual/ free or a wellness visit with a gynecologist usually does not have an associated co-pay. It covers only below items:

-

Pap test

-

Contraception counseling (counseling only – actual birth control may or may not be covered).

-

STD testing.

The biggest thing to remember is that the “free” part only applies to the visit, not to the cost of your prescription, lab tests etc.

You may still have co-insurance or deductible applicable towards the lab fees or prescription costs. Your health care provider has no way of knowing which lab charges will or will not be paid for by your carrier.

If you have any additional problems that require attention such as fibroids, irregular periods etc., you will be required to pay a co-pay and may require a separate visit.

Why can’t the healthcare provider bill my visit as a “preventative visit” so that my insurance can cover it a 100%

As mentioned above, any issue other than a pap, STD testing and contraceptive counseling is not a part of the preventative visit. The provider cannot commit fraud by not billing appropriately for the services rendered.

Each problem and each service has certain codes and the insurance company will decide reimbursement accordingly.

In fact, many health care providers may not address any additional problems at the time of a preventative visit and ask you to make a separate appointment since they may not get reimbursed for the additional issues discussed.

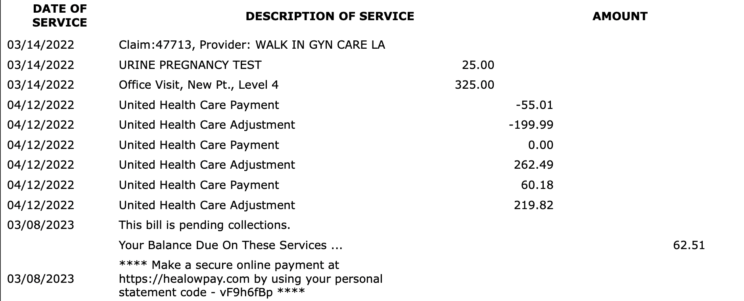

I keep getting bills. Where are they coming from?

You just went to the doctor or were at the hospital. You can get bills from many places.

Doctor’s office or the hospital bill

This will be an actual bill that you will need to pay. The breakdown of charges, insurance payments, adjustments may or may not be listed there. You may see a high amount listed under “charges”. That is not what the doctor or the hospital got paid. You will see the service fees listed usually in the far right column.

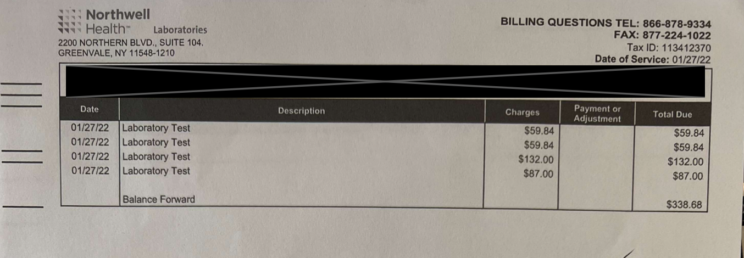

Lab Bill

The lab gets paid by your insurance separately. The lab has nothing to do with your doctor’s or the hospital bill. Your insurance plan may have different copays and deductibles for lab tests. You need to be aware of these costs yourself. Do you own research. A Covered test does not mean that you will not be responsible for your plan’s deductible or co-insurance.

I have a large bill. I asked my doctor to give me discount but they said they can’t. Why?

The health care provider has a contract with each insurance company. The insurance company decides the exact amounts that they will pay the provider based on that contract. It doesn’t matter what the provider charges, the insurance will pay only the contracted amount.

It is the responsibility of the health care provider to collect the contracted amounts (as applicable via the copay or deductibles). If the provider does not collect the balance payment, the insurance company and the law can construe that as a bribe. That is illegal and a breach of contract. Hence, once the insurance company has been billed, the claim has been processed and the bill has been generated, the health care provider cannot waive the bill.

The health care provider can help you with a payment plan depending on their rules.

How can I avoid large bills if I have a high deductible?

You have a choice to use your insurance or not. If you do not want to get a large bill due to a high deductible, you can choose not to use the insurance and just pay cash for the services.

Why doesn’t the doctor take my insurance?

The in-network participation status of your health care provider depends on many factors. Some insurance companies have a lot of providers so they close the networks for new providers. In other cases, the health care provider may not want to be in-network with certain insurances due to low reimbursements, delayed payments, denials etc. There is not much you can do but find an in-network health care provider if you want to use your insurance. You cannot force this on your provider.

I have out of network benefits. Can I see whoever I want?

If you have out of network benefits then you may be able to see the provider you want. In that case, you may receive the reimbursement check directly. It is your legal responsibility to provide that check to your provider. Alternatively, the health care provider may take fees from you upfront. Then you will get reimbursed either the entire amount or a portion from your insurance company.

Why does my insurance require prior authorization for certain drugs or tests?

The insurance carriers place limits on various tests and prescriptions to keep their costs low. They will want you to have tried generic or lower cost medications before they can approve more expensive or branded medications.

Same applies to diagnostic testing. For example, even though your plan may state that they cover annual mammograms, they might not cover breast sonograms (or ultrasounds) which may be needed if you have dense breasts or a suspected mass on a screening mammogram. In that case, they will require prior authorization for that additional testing.

Whose responsibility is it to get prior authorizations?

Some practices will assist in obtaining prior authorizations as a courtesy to their patients. However, it is not entirely under their purview to do so. You as a patient may have to get the test or medication approved by your insurance carrier yourself by providing proof as requested.

Why do I have to pay when I go to pick up my prescription even though I paid a co-pay at my doctor’s visit and pay a monthly premium?

Again, these are fine print costs that many are not aware of when signing up for a plan. Your pharmacy benefits may be entirely different from your office visit benefits.

How can I be a more informed consumer?

- READ: Read your entire benefits plan.

- LOOK: Be on the look-out for each of the below fees or percentages associated with each type of visit. Build your own cheat sheet as below.

- SHOP: Shop the market place and compare the below items and not just go for the lowest monthly premium.

- ASK: Ask questions: You are paying for your plan. You have the right to ask questions and reach out to your carrier.

| Office visit (PCP) | Office visit (specialist) | Referral required (Y/N) | ER visit | Hospital admission | Pharmacy | Lab/ Diagnostics | |

| Co-pay | |||||||

| Co-insurance | |||||||

| Deductible |

We are living in a very confusing place. There are hundreds of insurance carriers and each one of them have hundreds of sub-plans. Last year on NY market place alone, there were 1700 plans to choose from. It is almost impossible for you to be able to understand the fine print and nuances for each of them. However, having some basic knowledge will make you a more informed consumer and prepare you for this mind-boggling arena.

Be safe, be strong and be prepared,

Dr. Adeeti Gupta and the Walk IN GYN Team